First-time homebuyer mistakes in California are defined as preventable errors in contract management, financing, and budgeting that cost buyers thousands of dollars or their dream home entirely. California’s real estate market operates under state-specific rules, including the California Residential Purchase Agreement, CalHFA down payment assistance programs, and mandatory Loan Estimate disclosures, that create unique traps for unprepared buyers. Miss a contingency deadline and you forfeit your earnest money deposit. Underestimate closing costs and you arrive at the table short on cash. This guide covers the most common first home buying mistakes so you can close with confidence, not regret.

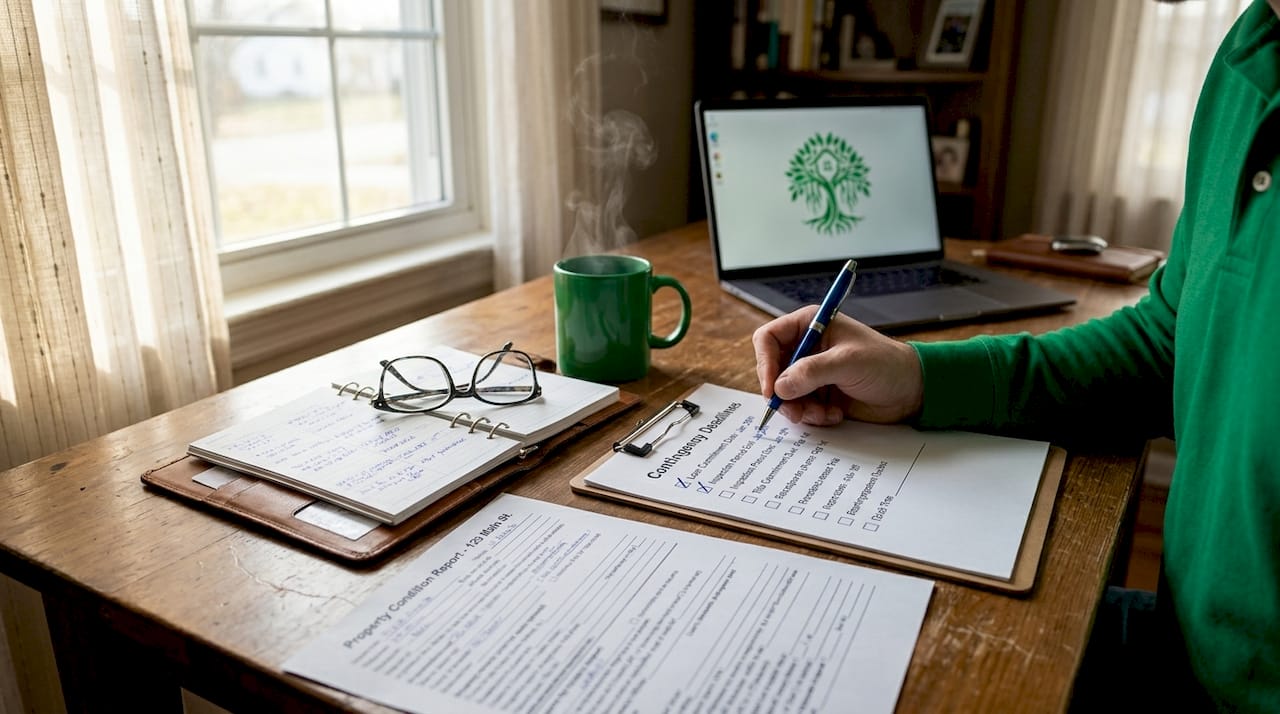

1. Mismanaging contingency deadlines in California

Contingency management is the single most misunderstood area for first-time buyers in California, and the financial consequences are severe. The California Residential Purchase Agreement sets specific deadlines for inspection, appraisal, and loan contingencies, and missing them does not just delay your purchase. It can cost you your deposit.

Here is what each contingency covers and when it typically expires:

- Inspection contingency: You must complete your home inspection and submit a written removal form, typically by day 17 after acceptance. Completing the inspection is not the same as removing the contingency in writing.

- Appraisal contingency: Protects you if the home appraises below the purchase price. Removal deadlines usually align with or follow the inspection window.

- Loan contingency: Gives you an exit if your financing falls through. This typically expires around day 21, though your contract may vary.

The critical trap here is assuming that doing the inspection automatically satisfies the contingency. It does not. Contingency removal requires a signed form submitted to escrow before the deadline. Buyers who skip this step can find themselves in default, with sellers legally entitled to cancel the contract and keep the deposit.

California also requires sellers to deliver disclosures like the Transfer Disclosure Statement (TDS) and Natural Hazard Disclosure (NHD) early in the transaction. Late disclosure delivery actually gives you the right to cancel or extend your contingency period, but only if you know to exercise that right.

One more risk that surprises buyers: wire fraud. California Civil Code Section 1057.3 requires you to independently verify escrow wiring instructions by phone before sending any funds. Never wire money based solely on an email, even one that looks official.

Pro Tip: Set calendar reminders for every contingency deadline the day you open escrow. Confirm with your escrow officer in writing that each removal form was received.

2. Underestimating cash needed to close

Most first-time buyers budget for the down payment and nothing else. That is a costly mistake in California’s high-price market. Closing costs in California average 3% to 6% of the loan amount and can exceed $17,581 depending on the purchase price. On a $700,000 home, that means you could owe an additional $21,000 to $42,000 at closing beyond your down payment.

California closing costs typically include:

- Lender fees: Origination charges, underwriting fees, and discount points

- Title and escrow fees: Title insurance, escrow service charges, and notary costs

- Prepaid items: Homeowners insurance premium, prepaid interest, and property tax reserves

- HOA fees: Transfer fees and any prorated dues if the property has a homeowners association

- Government fees: County recording fees and transfer taxes

A mistake many buyers make is comparing lenders only by interest rate. Full loan cost comparison including fees, points, and total cash to close is what actually determines which lender saves you money. Two lenders offering the same rate can differ by thousands in fees.

To reduce your cash-to-close burden, ask about seller concessions during negotiation. In a balanced or buyer-friendly market, sellers will sometimes credit you a portion of closing costs. CalHFA programs also offer down payment and closing cost assistance for qualifying first-time buyers, which can meaningfully reduce what you need to bring to the table.

Pro Tip: Request a Loan Estimate from at least three lenders and compare the “Closing Cost Details” section line by line, not just the interest rate.

3. Shopping for homes without a pre-approval

Pre-approval and pre-qualification are not the same thing, and confusing them is one of the most common first-time buyer pitfalls in California’s competitive market. Pre-qualification is an informal estimate based on self-reported income and assets. Pre-approval is a verified commitment from a lender based on your actual credit report, tax returns, pay stubs, and bank statements.

Lacking pre-approval weakens your offer significantly. California sellers, especially in markets like the Bay Area, Los Angeles, and San Diego, routinely receive multiple offers. A pre-qualified buyer looks uncertain next to a pre-approved buyer. In many cases, listing agents will advise their sellers to reject or deprioritize offers without a pre-approval letter.

What pre-approval requires from you:

- Two years of W-2s or tax returns (three years if self-employed)

- Recent pay stubs covering the last 30 days

- Two to three months of bank and investment account statements

- A hard credit pull, which temporarily affects your score by a few points

- Explanation letters for any large deposits or credit inquiries

Pro Tip: If you are exploring CalHFA or other assistance programs, confirm your lender is an approved CalHFA lender before starting the pre-approval process. Not every lender participates, and switching mid-process delays your timeline.

4. Assuming you need 20% down

The 20% down payment requirement is a myth that stops many first-time buyers from even starting their search. FHA loans and other programs allow significantly smaller down payments, and California has several state-specific options that make homeownership accessible at lower entry points.

Your actual options as a California first-time buyer include:

- FHA loans: 3.5% down with a credit score of 580 or higher; 10% down with scores between 500 and 579

- Conventional 97 loans: 3% down for qualifying borrowers through Fannie Mae or Freddie Mac programs

- CalHFA MyHome Assistance Program: Provides a deferred-payment junior loan to cover down payment or closing costs

- VA loans: 0% down for eligible veterans and active-duty service members

- USDA loans: 0% down for properties in designated rural areas of California

The trade-off with smaller down payments is mortgage insurance. FHA loans require both an upfront mortgage insurance premium and an annual premium. Conventional loans with less than 20% down require private mortgage insurance (PMI), which cancels once you reach 20% equity. Understanding these costs upfront prevents sticker shock on your monthly payment.

Your credit score and debt-to-income ratio determine which programs you qualify for, so reviewing both before you apply gives you a clearer picture of your real options.

5. Ignoring the full monthly housing cost

Budgeting only for principal and interest is one of the most persistent common homebuyer errors in California. True monthly housing costs include property taxes, homeowners insurance, mortgage insurance, HOA dues, and sometimes special assessments. In California, these additions can push your actual monthly payment 30% to 50% above the mortgage payment alone.

| Cost component | What to expect in California |

|---|---|

| Property taxes | Roughly 1.1% to 1.25% of assessed value annually under Proposition 13 |

| Homeowners insurance | Rising sharply due to wildfire risk; some insurers have exited the state entirely |

| HOA dues | Range from $200 to over $1,000 per month depending on community |

| Special assessments | One-time charges for major repairs or improvements in HOA communities |

| Mortgage insurance | Required on FHA loans and conventional loans with less than 20% down |

California’s wildfire insurance crisis deserves specific attention. Insurers including State Farm and Allstate have paused or restricted new policies in high-risk ZIP codes. Before making an offer, verify that the property is insurable and get an actual insurance quote, not an estimate. Some buyers have closed on homes only to discover their insurance costs were two to three times what they expected.

Use a mortgage payment calculator that includes taxes and insurance to model your real monthly obligation before you fall in love with a listing.

Pro Tip: Ask the listing agent for the current HOA budget and reserve study. A low HOA fee backed by an underfunded reserve often means a special assessment is coming.

6. Skipping a thorough review of seller disclosures

California requires sellers to provide more disclosures than almost any other state, and first-time buyers often skim them or skip them entirely. That is a serious mistake. The Transfer Disclosure Statement, Natural Hazard Disclosure, and supplemental disclosures cover everything from past water damage and unpermitted additions to flood zones and seismic hazards.

Early receipt and review of seller disclosures protects your right to cancel or renegotiate before contingency deadlines expire. If disclosures arrive late, California law gives you the right to extend your contingency period or cancel without penalty. But you can only exercise that right if you know it exists and act within the proper timeframe.

Read the full California buyer disclosure guide before you open escrow. Pay particular attention to any items the seller marks as “unknown” rather than “no.” Unknown responses on a TDS often signal issues the seller suspects but cannot confirm, and those are worth investigating further during your inspection period.

Key takeaways

Avoiding first-time homebuyer mistakes in California requires mastering contingency deadlines, budgeting for full closing costs, securing pre-approval before you search, and understanding every component of your monthly payment.

| Point | Details |

|---|---|

| Contingency deadlines are binding | Submit signed removal forms before each deadline or risk losing your deposit. |

| Closing costs exceed expectations | Budget 3% to 6% of the loan amount on top of your down payment in California. |

| Pre-approval beats pre-qualification | Only a verified pre-approval letter strengthens your offer in competitive markets. |

| 20% down is not required | FHA, CalHFA, and conventional programs allow 3% to 3.5% down for qualified buyers. |

| Full monthly costs matter | Factor in property taxes, insurance, HOA dues, and PMI before committing to a price. |

What I’ve learned watching buyers navigate California real estate

I have seen buyers lose $15,000 deposits not because they were careless, but because nobody told them that completing an inspection and removing an inspection contingency are two completely different actions. California’s purchase agreement is detailed and unforgiving, and the pressure to compete in a fast-moving market pushes buyers to waive protections they do not fully understand.

The 20% down myth is equally damaging. I have watched qualified buyers sit on the sidelines for years, saving toward a threshold they did not need to hit, while home prices moved further out of reach. CalHFA and FHA programs exist precisely for this situation, and most buyers I talk to have never heard of them until they are already deep into the process.

My honest advice: treat your contingency calendar like a legal obligation, because it is one. Get your full Loan Estimate before you commit to a lender, not after. And before you make an offer on any property, get an actual insurance quote for that specific address. In California’s current insurance market, that single step can save you from a very expensive surprise.

The buyers who close successfully are not the ones with the most money. They are the ones who asked the right questions early and had a clear picture of what they were signing. Use the first-time homebuyer guide from Ficustree to build that foundation before you start touring homes.

— Anand

How Ficustree helps you avoid these mistakes from day one

Ficustree is an AI-powered real estate platform built specifically for first-time California homebuyers. It guides you from your first search to closing on a single platform, with tools designed to prevent the exact mistakes covered in this article.

Use Ficustree’s home affordability calculator to model your true monthly payment including taxes, insurance, and HOA dues before you fall for a listing. The platform surfaces CalHFA-approved lenders, flags contingency deadlines, and connects you with educational resources on every step of the California purchase process. Whether you are trying to understand closing costs or figure out how much you actually need to bring to the table, Ficustree gives you the clarity to move forward with confidence. Start your search and see how much easier buying your first home can be.

FAQ

What are the most common first-time homebuyer mistakes in California?

The most common mistakes include missing contingency removal deadlines, underestimating closing costs, shopping without a pre-approval letter, assuming a 20% down payment is required, and failing to budget for property taxes, insurance, and HOA dues.

How much should I budget for closing costs in California?

Closing costs in California average 3% to 6% of the loan amount, which can exceed $17,581 on higher-priced homes. Budget for this separately from your down payment.

What happens if I miss a contingency deadline in California?

Missing a contingency deadline without submitting a signed removal form can put you in default under the California Residential Purchase Agreement. The seller may have the right to cancel the contract and keep your earnest money deposit.

Do I need 20% down to buy a home in California?

No. FHA loans require as little as 3.5% down, and CalHFA programs offer additional assistance for qualifying first-time buyers. Conventional loan programs through Fannie Mae and Freddie Mac also allow 3% down.

Why is pre-approval more important than pre-qualification in California?

Pre-approval is based on verified financial documents and a hard credit check, which makes your offer credible to sellers. Pre-qualification is an informal estimate that carries little weight in California’s competitive markets where sellers routinely compare multiple offers.