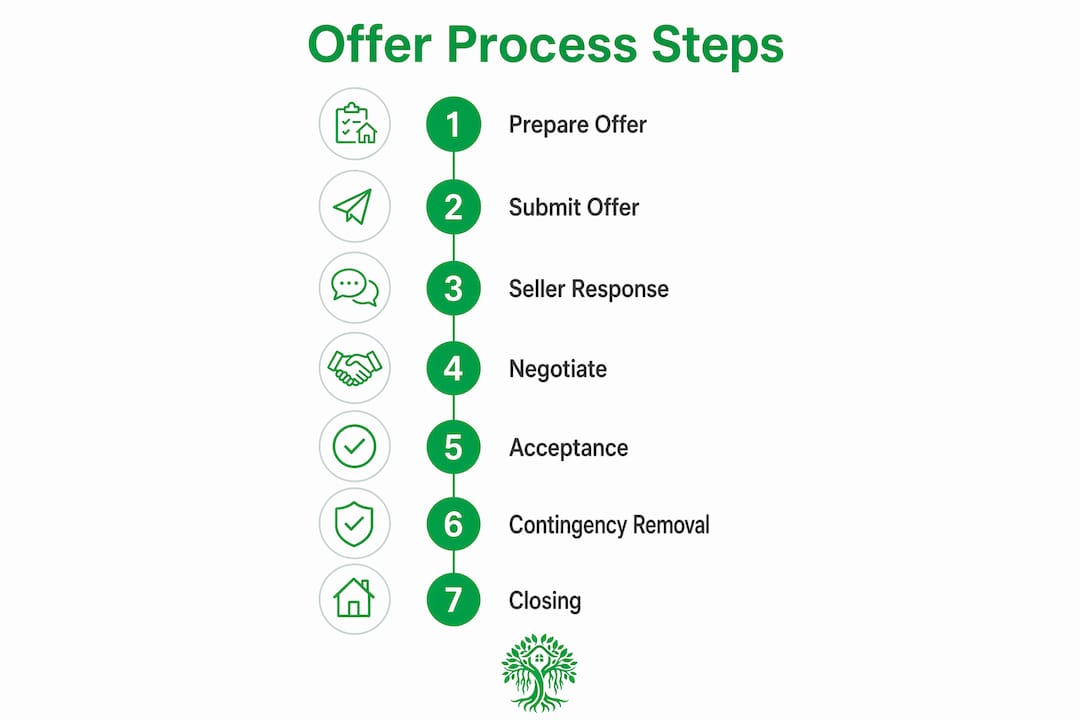

The real estate offer process is the step-by-step procedure where a buyer submits a formal written proposal to purchase a home, the seller responds by accepting, rejecting, or countering, and both parties negotiate until they reach a legally binding agreement. For first-time buyers in California, understanding how this process works is the difference between a confident, protected purchase and a costly mistake. California’s legal framework adds specific requirements around contract delivery, contingency deadlines, and earnest money that you won’t find in most other states. This guide walks you through every stage, from submitting your first offer to closing day.

How the real estate offer process works in California

The formal term for your written offer in California is the California Residential Purchase Agreement, or RPA. Published by the California Association of Realtors (C.A.R.), the RPA is the standard contract used in nearly every residential transaction across the state. It covers purchase price, contingencies, closing timeline, and dozens of other terms that define your rights as a buyer.

One fact that surprises many first-time buyers: signing the offer yourself does not make the deal binding. In California, your offer becomes legally binding only when both parties have signed and a copy has been delivered to the buyer. That delivery requirement is unique and matters enormously. Until that moment, either party can walk away without legal consequence.

The key players in this process are the buyer, the seller, and their respective real estate agents. Your agent submits the offer package on your behalf through a licensed broker. The seller’s agent presents it to the seller, who then has a set window to respond.

What happens when you submit a real estate offer

Your offer package is more than just a price. A complete submission through the RPA typically includes:

- Purchase price and the financing terms you’re relying on

- Earnest money deposit amount and the timeline for delivery

- Contingencies covering inspection, appraisal, and loan approval

- Proposed closing date, usually 30 to 45 days from acceptance

- Proof of funds or preapproval letter from your lender

Earnest money deposits in California typically range from 1% to 3% of the purchase price, due within 3 business days of acceptance. In competitive Bay Area or Los Angeles markets, buyers sometimes offer 5% to 10% to signal serious intent. That deposit is refundable while contingencies are active, but it becomes at risk the moment you remove them.

A complete offer package submitted as a single, organized PDF with all documentation reduces seller hesitation and avoids back-and-forth delays. Sellers in competitive markets treat incomplete packages as a red flag. Your preapproval letter, proof of funds, and signed RPA should all arrive together.

Pro Tip: Ask your lender for an updated preapproval letter dated within the last 30 days. Sellers and their agents notice the date, and a fresh letter signals you’re actively ready to buy, not just browsing.

How sellers respond: acceptance, rejection, and counteroffers

Once your offer lands, the seller has three options. They can accept your terms as written, reject the offer outright, or issue a counteroffer. Most transactions in California involve at least one round of negotiation before both sides agree.

Counteroffers typically adjust one or more of these terms:

- Purchase price, either higher or lower than your initial bid

- Earnest money deposit, often increased to reduce seller risk

- Closing date, adjusted to fit the seller’s moving timeline

- Contingency terms, such as shortening the inspection period

When you receive a counteroffer, you have the same three options the seller had: accept, reject, or counter again. This back-and-forth continues until both parties agree on every term or one side walks away. There is no legal limit on the number of rounds, but most negotiations resolve within two or three exchanges.

Understanding seller priorities in competitive markets helps you respond strategically. Sellers weigh certainty and risk as much as price. A buyer offering $10,000 less with a clean preapproval and flexible closing date often beats a higher offer loaded with contingencies. When evaluating a counteroffer, focus on the total risk picture, not just the number. You can also learn more about asking for seller concessions when the negotiation moves in your favor.

What are contingencies and why do they matter?

Contingencies are conditions written into the RPA that allow you to cancel the contract and recover your earnest money if specific situations arise. They are your primary legal protection as a buyer, and California law takes them seriously.

The three most common contingencies in California residential transactions are:

- Inspection contingency: Gives you the right to have the property professionally inspected and to cancel or renegotiate based on findings. The standard timeline under the RPA is 17 days from acceptance.

- Appraisal contingency: Protects you if the home appraises below the purchase price. Also typically 17 days. Without this, you’re on the hook to cover any gap between the appraised value and your offer price.

- Loan contingency: Allows you to cancel if your lender cannot approve your financing. Loan contingencies run approximately 21 days from acceptance under the standard RPA.

Here is where many first-time buyers make a critical error. Completing your inspection does not automatically remove the inspection contingency. You must submit a written contingency removal form by the deadline. If you miss that deadline, you risk losing your earnest money even if you never intended to waive your rights. The contract operates on written acts and delivery, not assumptions or verbal agreements.

Pro Tip: Set calendar reminders for every contingency deadline the moment your offer is accepted. Missing a removal deadline by even one day can shift your deposit from protected to at risk. Your agent should track these, but you should track them too.

California law also gives buyers statutory rights tied to seller disclosures, including the Transfer Disclosure Statement. These disclosures can extend your cancellation window beyond the standard contingency period, giving you additional protection if the seller reveals material defects late in the process. Review the California buyer disclosures guide to understand exactly what you’re entitled to receive and when.

What happens after offer acceptance

Acceptance triggers a series of deadlines that run simultaneously. Managing them well is what separates a smooth closing from a stressful one.

Here is what typically happens in the 30 to 45 days between acceptance and closing:

- Days 1 to 3: Deliver your earnest money deposit to escrow

- Days 1 to 5: Submit your full loan application to your lender

- Days 1 to 17: Schedule and complete your home inspection and appraisal

- Days 17 to 21: Submit written contingency removals as each deadline passes

- Days 21 to 30: Lender orders title report, underwriting begins

- Days 30 to 45: Final walkthrough, loan funding, and closing

The RPA contract dates are your source of truth. Every deadline flows from the acceptance date, not the calendar date you signed. Cash buyers can often close in 10 to 14 days because they skip the loan approval timeline entirely. If you’re financing, your lender’s speed directly affects whether you close on time.

Coordination between your escrow officer, lender, and agent is constant during this phase. A delay from any one party can push your closing date and potentially trigger contract penalties. Stay in contact with all three at least twice a week.

Strategies for making a competitive offer in California

California’s housing market, particularly in cities like San Francisco, San Jose, Los Angeles, and San Diego, regularly produces multiple-offer situations. Price alone rarely wins. Here is how different offer strategies compare:

| Strategy | What it signals to the seller | Risk to buyer |

|---|---|---|

| Higher earnest money (5%+) | Strong commitment, financial stability | Deposit at risk if contingencies waived |

| Flexible closing date | Reduces seller’s logistical stress | Minor scheduling inconvenience |

| Shorter contingency periods | Faster deal certainty for seller | Less time to uncover property issues |

| Escalation clause | Automatic price increase over competing offers | May overpay if not capped carefully |

| Clean preapproval letter | Reduces financing risk perception | None, always recommended |

In multiple-offer situations, sellers weigh risk and certainty alongside price. A preapproval from a well-known lender like Wells Fargo or a local credit union carries more weight than a generic online prequalification. Acting quickly also matters. Homes in competitive California zip codes often receive offers within 48 to 72 hours of listing. Waiting three days to “think about it” frequently means losing the property.

Escalation clauses can give you an edge without blindly overbidding. You set a base offer price, a maximum cap, and an increment above any competing offer. For example, $850,000 base, escalating $5,000 above any competing offer, up to $900,000. This approach is covered in detail in the competitive offer strategies guide from Lo Fi Rate.

Key takeaways

The real estate offer process in California requires written acts, precise deadlines, and strategic positioning at every stage, from the initial RPA submission through contingency removal and closing.

| Point | Details |

|---|---|

| Binding moment requires delivery | Your offer is not legally binding until both parties sign and a copy is delivered to the buyer. |

| Earnest money becomes at risk | Deposits of 1% to 3% are refundable during contingencies but become at risk after written removal. |

| Written removal is mandatory | Completing an inspection does not remove the contingency. You must submit a written removal form by the deadline. |

| Sellers value certainty over price | Strong preapproval, flexible closing dates, and higher deposits often outperform higher prices in competitive markets. |

| Post-acceptance timeline is tight | Most California closings run 30 to 45 days, with simultaneous deadlines for inspections, appraisals, and loan approval. |

What I’ve learned watching first-time buyers navigate California offers

Most first-time buyers focus almost entirely on price. That’s understandable. But in my experience, the buyers who run into serious trouble are almost never the ones who offered too little. They’re the ones who missed a contingency removal deadline, submitted an incomplete offer package, or didn’t understand that their deposit was no longer protected the moment they signed that removal form.

California’s RPA is a detailed contract, and it rewards buyers who treat it that way. I’ve seen buyers lose their full earnest money deposit, sometimes $15,000 to $25,000, because they assumed their agent had submitted the removal paperwork when it hadn’t been filed. That’s not a price negotiation problem. That’s a deadline management problem.

The other pattern I see consistently: buyers who work closely with their lender before submitting an offer, not after. Getting a full underwriting approval rather than a basic prequalification changes how sellers perceive your offer. It’s the single highest-leverage move a first-time buyer can make before writing a single dollar on the RPA.

California’s market in 2026 continues to reward preparation and speed. The buyers who win are the ones who understand the process before they need it, not while they’re in the middle of it.

— Anand

How Ficustree helps you submit stronger offers

Ficustree is an AI-powered home buying platform built specifically for first-time buyers in California. From your first property search to the moment you close, Ficustree keeps your offer timeline, contingency deadlines, and negotiation data in one place.

The platform gives you real-time market data to inform your offer price, tracks every RPA deadline automatically, and surfaces seller responsiveness signals that help you time your submission. You won’t need to chase your agent for updates or build your own spreadsheet to track contingency dates. Ficustree does that work for you. If you’re preparing to make your first offer in California, explore the Ficustree buyer platform and see how AI-guided support changes the experience. You can also learn more about how Ficustree works and what makes it different from a traditional home search.

FAQ

When does a real estate offer become legally binding in California?

A real estate offer in California becomes legally binding only when both the buyer and seller have signed the agreement and a copy has been delivered to the buyer. Signing alone is not sufficient under California law.

How much earnest money should I offer in California?

Standard earnest money deposits range from 1% to 3% of the purchase price, due within 3 business days of acceptance. In competitive markets like the Bay Area or Los Angeles, deposits of 5% or more are common.

What is a contingency removal in California?

A contingency removal is a written form submitted by the buyer that formally waives a specific protection, such as the inspection or loan contingency. Completing an inspection does not remove the contingency. The written form must be submitted by the RPA deadline.

How long does it take to close after offer acceptance in California?

Most California closings take 30 to 45 days from acceptance when financing is involved. Cash buyers can often close in 10 to 14 days because they skip the loan underwriting timeline.

What happens if a seller rejects my offer?

If a seller rejects your offer outright, you are free to submit a new offer or move on to another property. A rejection is not a counteroffer, and your earnest money is not at risk since no contract was formed.