Buying a home is exciting. However, it also comes with one question that almost every buyer worries about: what is the true cost of homeownership, and how much can I actually afford without putting my life under pressure?

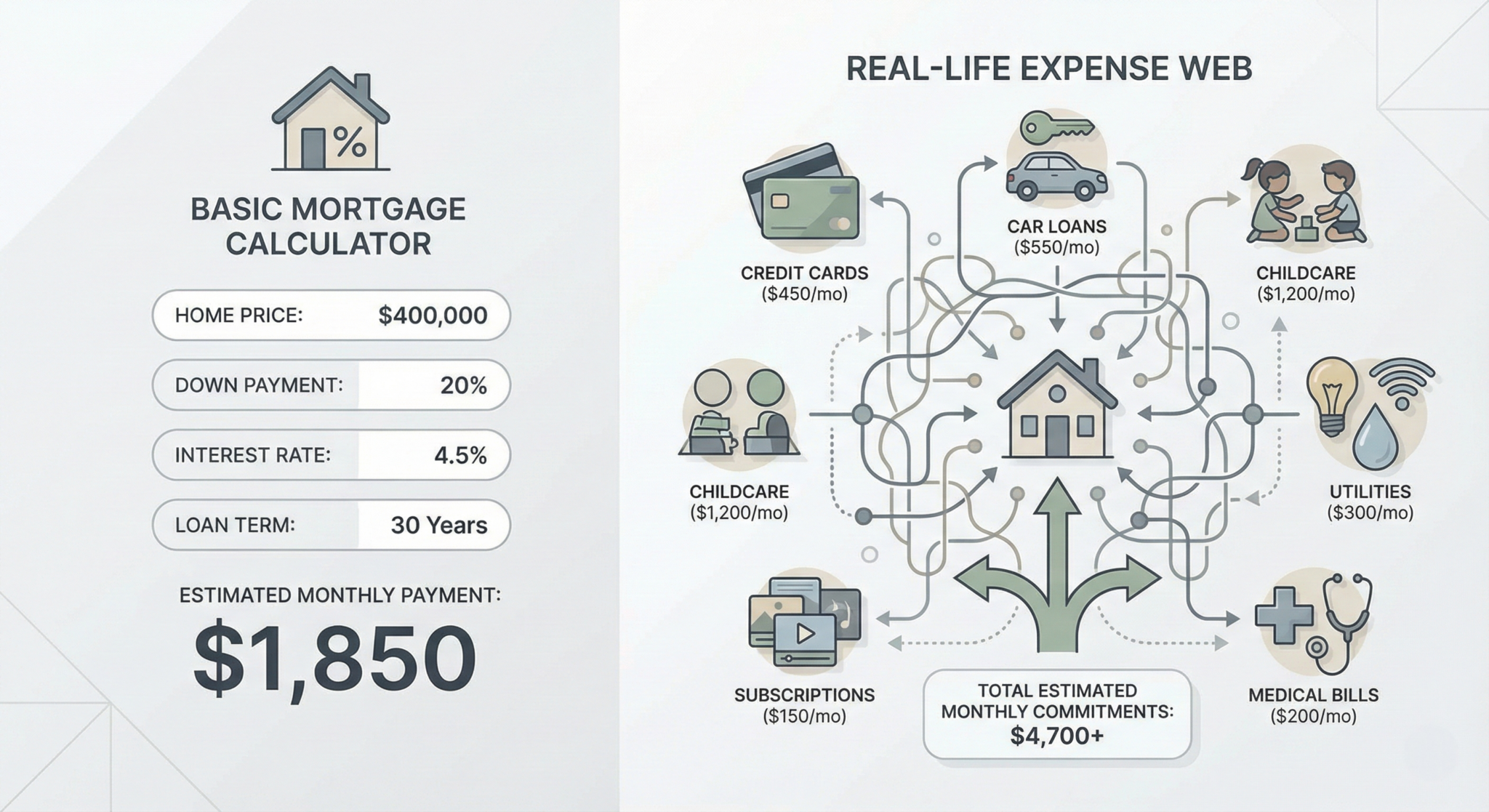

Most buyers begin with a mortgage calculator. It shows a monthly payment, property taxes, and sometimes HOA fees. At first glance, everything seems manageable. Yet real life is never that simple. Your budget is shaped by credit cards, auto loans, family expenses, utilities, repairs, lifestyle costs, and other monthly home expenses that traditional calculators never include.

Because of this gap, many buyers feel confident on paper but stressed after they move in. We built ficustree to avoid such situation to our users. We believe buyers deserve a clear and realistic view of affordability, not a quick math that ignores real life.

Why Simple Affordability Calculators Miss the Real Picture

Traditional affordability calculators focus on the loan. Unfortunately, they ignore the financial commitments you already carry every month.

Most calculators leave out costs such as:

- Credit card minimum payments

- Auto loans

- Student loans

- Personal or medical loans

- Childcare expenses

- Subscriptions and recurring services

- Insurance premiums

- Monthly lifestyle spending

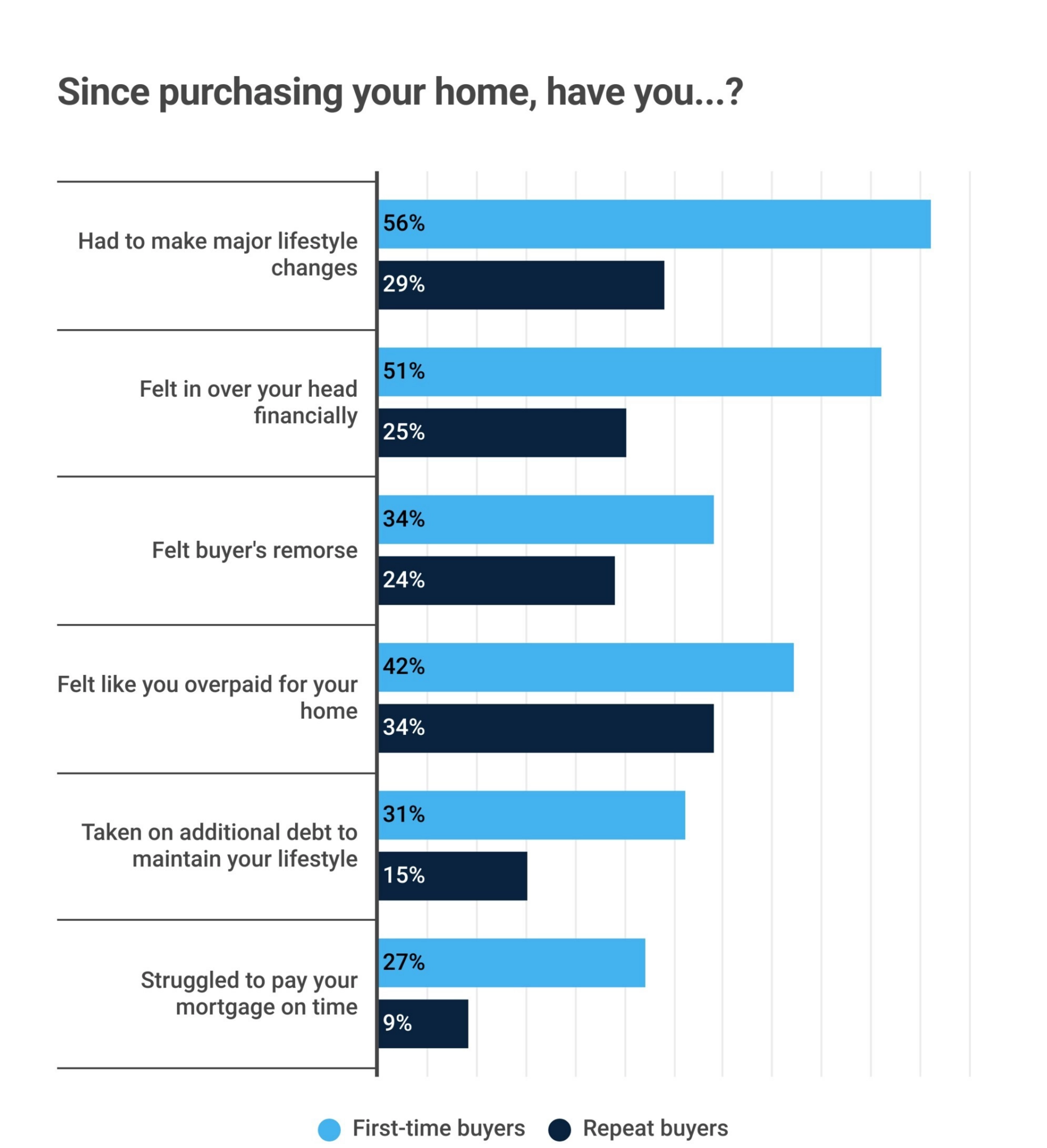

As a result, buyers often believe they can afford a home that technically fits the formula but does not fit their day-to-day life. According to prnewswire 51% of first-time home buyers felt the jolt.

Ficustree helps buyers understand the financial factors that truly affect comfort and stability, not just approval limits.

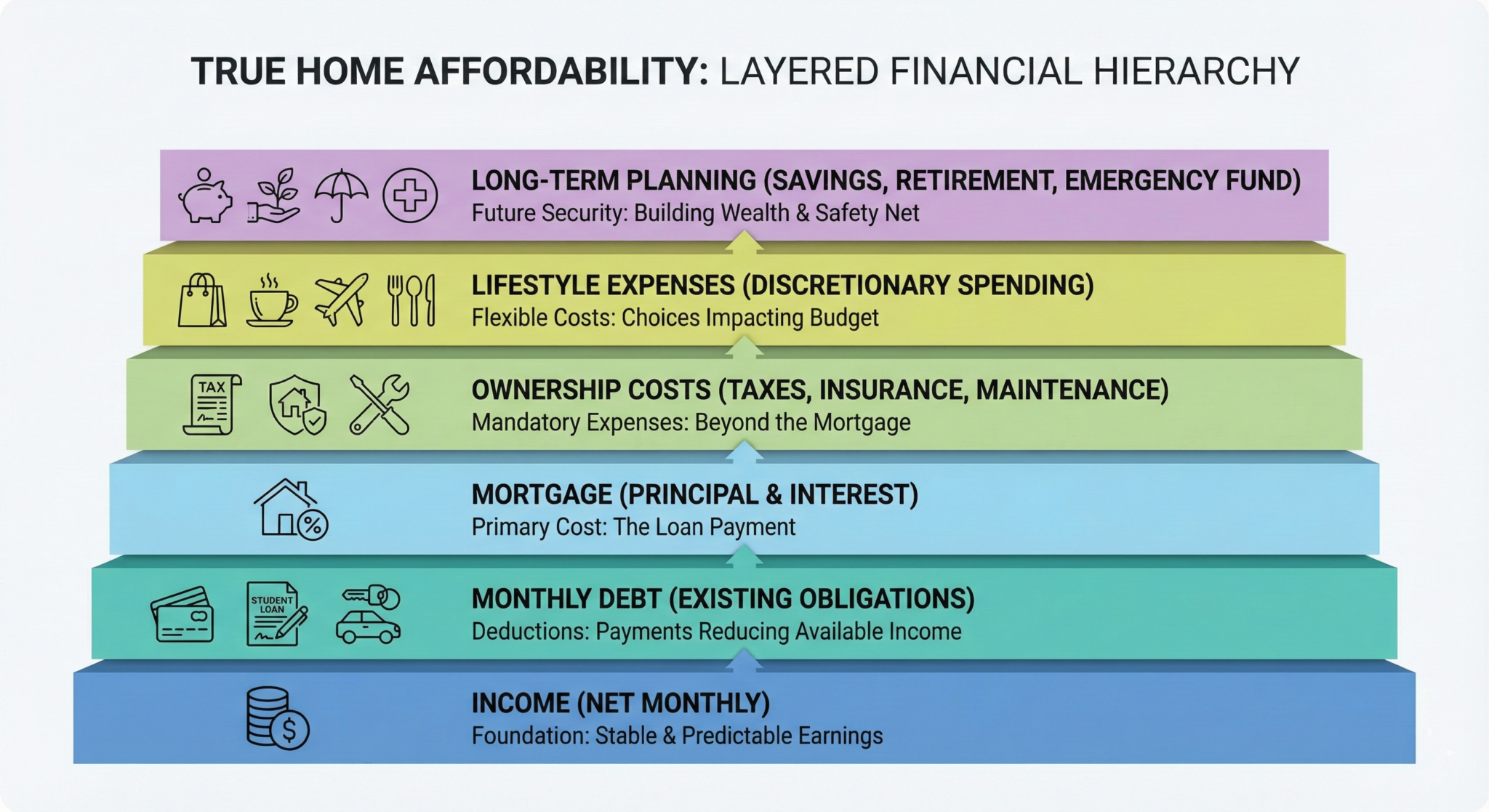

What the True Cost of Homeownership Really Includes

Understanding the true cost of homeownership means looking at the full financial picture, not just the mortgage.

1. Your Total Monthly Debt

A realistic affordability calculation starts with your actual obligations. This includes:

- Credit card minimums

- Car payments

- Student loans

- Personal or consolidation loans

- Current rent or mortgage

- Child support or alimony

- Medical payments

- Subscriptions and lifestyle expenses

When you account for these first, you see how much room you truly have for a home.

2. Your Future Mortgage, Based on Real Loan Details

Instead of using estimates, buyers should calculate affordability using real loan assumptions, such as:

- Loan amount

- Type of loan, including Conventional, FHA, or VA

- Loan term, such as 15 or 30 years

- Interest rate

- Discount points, if applicable

- Down payment

- PMI, when required

This ensures your mortgage estimate reflects your actual plan, not a generic scenario.

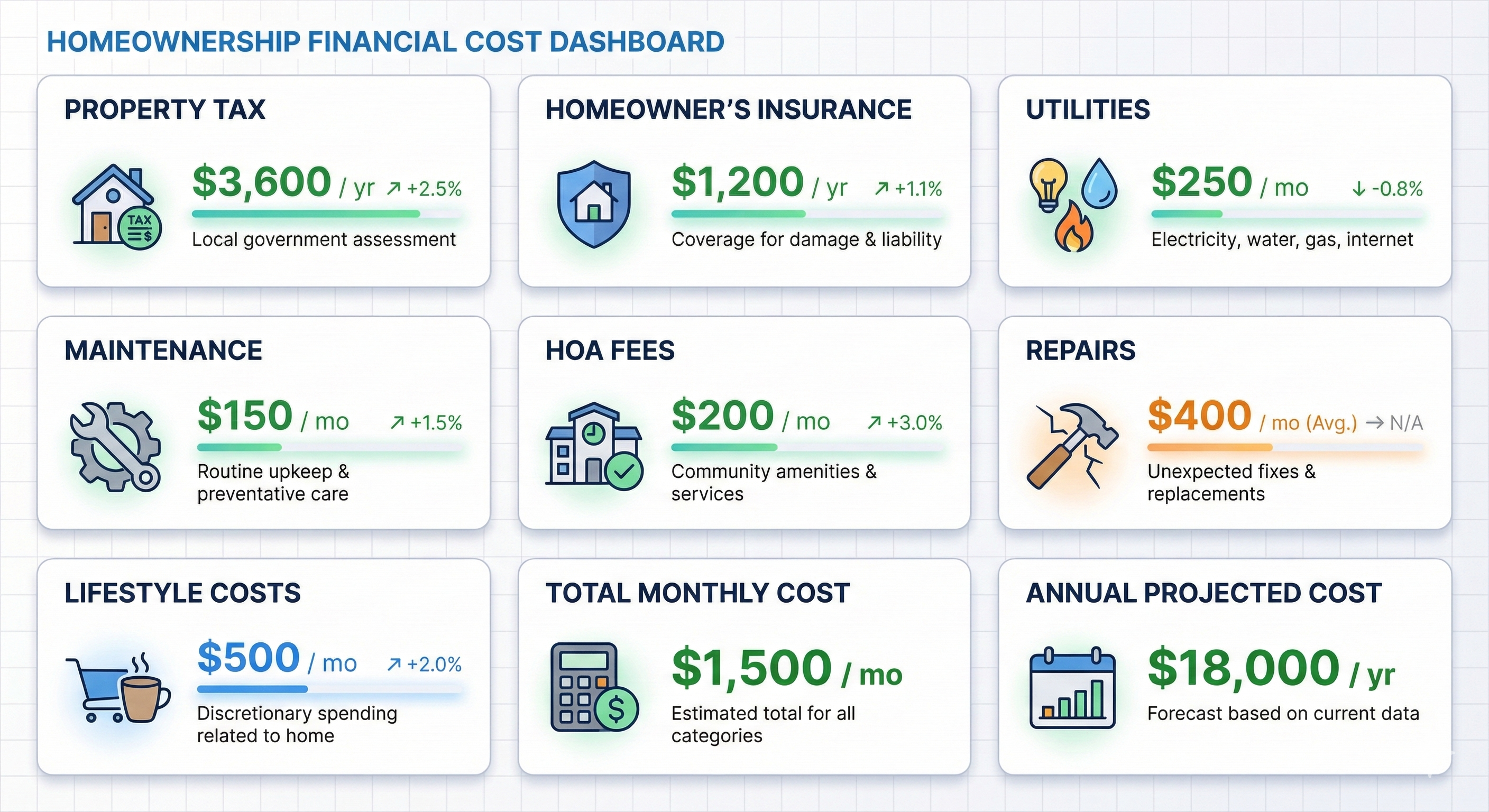

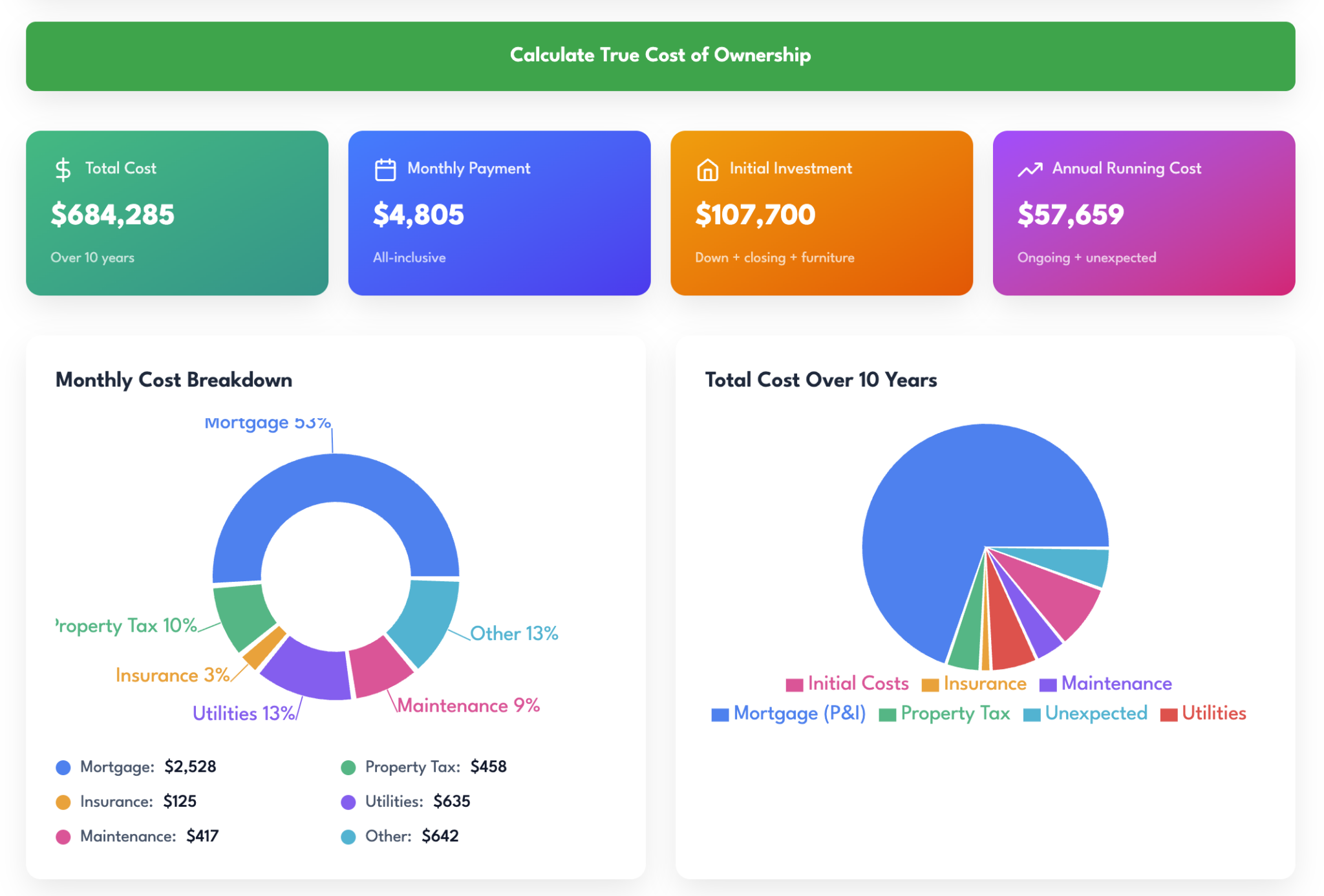

3. Real Homeownership Costs Most Buyers Forget

Owning a home comes with ongoing expenses beyond the monthly loan payment. Planning for these costs upfront helps avoid surprises later.

Core monthly and yearly costs

- Property taxes

- Homeowners insurance

- HOA fees

- Utilities such as water, electricity, gas, and trash

- Internet services

- Yard maintenance

- Pest control

Maintenance and unexpected repairs

Every home ages. Systems wear out, and appliances eventually fail. Buyers should consider:

- Roof age and replacement timelines

- HVAC life expectancy

- Water heater condition

- Appliance age

- Plumbing and electrical systems

- Flooring and windows

- Typical repair costs for the area

- Annual maintenance savings

Location and lifestyle factors

- Commute expenses

- School activities

- Community fees

- Parking or EV charging

- Local cost of essentials

All of these influence whether a home feels comfortable or financially stressful.

4. Closing Costs Many Buyers Overlook

Upfront costs often surprise buyers, especially first-time buyers. These may include:

- Lender fees

- Title and escrow charges

- Appraisal fees

- Recording fees

- Transfer taxes

- Home inspections

- Moving expenses

Together, these costs can add thousands to your initial budget.

5. How Your Finances Look After You Buy

Affordability is not about buying the biggest home the bank approves. Instead, it is about living comfortably after closing.

That is why buyers should think about:

- Remaining savings after purchase

- Emergency funds

- Monthly savings potential

- Future repairs

- Property tax increases

- Insurance changes

- Utility cost shifts

- Long-term resale value

This creates a five to ten year view of affordability, not just the first month.

How ficustree Helps Buyers Understand the True Cost of Homeownership

The ficustree affordability experience starts with you, not the listing. By understanding your financial details, lifestyle needs, and future plans, ficustree helps buyers find homes that are truly affordable.

Buyers work with a personalized AI agent that considers real debt, ownership costs, and long-term impact. This approach helps buyers choose homes they can enjoy for years without financial strain.

Why the True Cost of Homeownership Matters

A complete affordability calculation helps prevent:

- Becoming house poor

- Unexpected financial pressure

- Costly repair shocks

- Feeling trapped by a mortgage

- Strain on family and lifestyle

- Delays in future goals

The right home should feel like freedom, not a burden.

The ficustree Approach to Real Affordability

ficustree is built for buyers, not for selling leads or pushing listings. Our approach focuses on:

- A realistic, debt-aware affordability view

- A complete breakdown of homeownership costs

- Long-term cost forecasting

- Personalized guidance based on lifestyle and future needs

We want every buyer to feel confident, informed, and secure in the home they choose.

The only calculator you need

If you are planning to buy a home, give yourself clarity beyond a basic calculator.

Your home should support your life, not limit it.

ficustree helps you understand the true cost of homeownership so you can choose a home that fits your budget, your goals, and your future.

Have a question? Find answers here…

What is the true cost of homeownership?

The true cost of homeownership includes far more than your monthly mortgage. It combines your loan payment, property taxes, insurance, utilities, maintenance, repairs, lifestyle expenses, and your existing financial obligations like loans and subscriptions.

Understanding this full picture helps buyers avoid financial stress after moving in.

Why do most traditional affordability calculators give misleading results?

Most calculators focus only on mortgage payments and ignore real-life expenses such as credit cards, auto loans, childcare, and lifestyle spending.

This creates a gap between what you’re approved for and what you can actually afford comfortably.

How much home can I realistically afford?

Real affordability depends on your total financial picture — income, existing debt, lifestyle costs, and long-term goals.

A home is affordable only if you can comfortably manage all expenses after buying, not just qualify for the loan.

What monthly costs should I consider beyond my mortgage?

Beyond your mortgage, you should account for:

- Property taxes

- Homeowners insurance

- Utilities

- HOA fees

- Internet and services

- Maintenance and repairs

These ongoing costs significantly impact your monthly budget.

What hidden costs of buying a home do buyers often miss?

Many buyers overlook:

- Closing costs (lender, escrow, appraisal fees)

- Moving expenses

- Immediate repairs or upgrades

- Maintenance reserves

These upfront costs can add thousands to your budget.

Why is it important to consider existing debt before buying a home?

Your current financial commitments such as loans, subscriptions, and childcare directly reduce how much you can comfortably spend on housing.

Ignoring these can lead to becoming “house poor.”

What are ongoing homeownership costs that increase over time?

Costs that can rise include:

- Property taxes

- Insurance premiums

- Utility costs

- Maintenance and repairs

- HOA fees

Planning for increases helps maintain long-term financial stability.

How much should I budget for home maintenance and repairs?

A common rule is to set aside 1–3% of the home value annually, but this varies based on the home’s age and condition.

Older systems like roofs, HVAC, and plumbing can significantly increase costs.

What is included in a realistic home affordability calculation?

A realistic calculation includes:

- Income and savings

- Total monthly debt

- Loan details (rate, term, PMI)

- Ongoing ownership costs

- Lifestyle and future expenses

This gives a complete affordability view, not just approval limits.

Why do some buyers feel financially stressed after buying a home?

Many buyers rely on simplified calculations and underestimate real expenses.

As a result, their monthly budget becomes tight, leading to stress, delayed goals, or lifestyle compromises.

How do lifestyle factors impact home affordability?

Factors like commute costs, school needs, community fees, and daily living expenses directly affect your overall budget and long-term comfort in a home.

How should I evaluate affordability over the long term?

Buyers should think beyond the first month and consider:

- Savings after purchase

- Emergency funds

- Future repairs

- Cost increases

- Resale value

This creates a sustainable 5–10 year financial outlook.