Escrow is defined as a neutral third-party arrangement where a licensed escrow officer holds your funds, documents, and deed until every condition of your purchase contract is satisfied. For first-time buyers in California, understanding the escrow process is the difference between a confident closing and a stressful scramble. This guide walks you through every step, clarifies who does what, and prepares you for the surprises most buyers never see coming, including escrow shortages and fluctuating monthly payments.

How does the escrow process work step by step for first-time buyers?

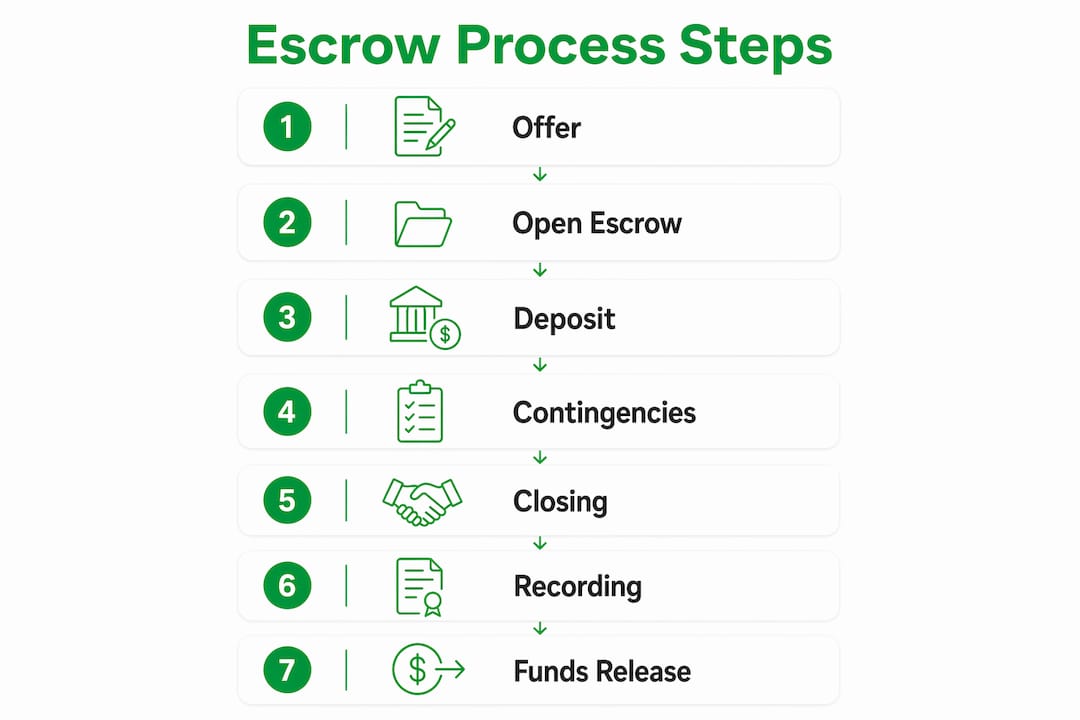

The escrow process for first-time buyers in California follows a clear sequence once your offer is accepted. Knowing each phase in advance removes the anxiety of waiting for news you don’t understand.

-

Open escrow. Your real estate agent or the seller’s agent contacts a licensed escrow company, such as First American or Fidelity National Title, to open escrow. The escrow officer receives a copy of the signed purchase agreement and begins coordinating all parties.

-

Deposit earnest money. You wire your earnest money deposit, typically 1% to 3% of the purchase price, into the escrow account within three business days of acceptance. On a $750,000 California home, that means $7,500 to $22,500 held securely until closing.

-

Complete inspections and disclosures. Your agent schedules a home inspection, and the seller delivers required California disclosures, including the Transfer Disclosure Statement and Natural Hazard Disclosure. You review these carefully and decide whether to request repairs or credits.

-

Title search and insurance. The escrow officer orders a title search to confirm the seller has clear ownership and no undisclosed liens exist. You then purchase a title insurance policy to protect against any future claims.

-

Lender coordination. Your mortgage lender orders an appraisal, processes your loan, and sends loan instructions directly to the escrow officer. You provide any additional documents your lender requests, such as updated pay stubs or bank statements.

-

Remove contingencies. Once inspections, financing, and appraisal are resolved, you sign contingency removal forms. This is a critical moment: removing contingencies means your earnest money is at risk if you back out without cause.

-

Sign closing documents and fund. You visit the escrow office or use a remote online notary to sign your loan documents. Your lender wires the loan funds, and you wire your down payment and closing costs to escrow.

-

Recording and possession. The escrow officer sends the deed to the county recorder. Once recorded, escrow closes and you receive your keys.

The standard escrow period runs 30 to 60 days in California, though cash purchases can close in as few as 10 days. Budget your schedule accordingly, especially if you are coordinating a lease end date.

Pro Tip: Set a calendar reminder for every escrow deadline in your purchase contract. Missing a contingency removal date by even one day can put your earnest money at risk.

What roles do escrow officers, lenders, and agents play?

Three distinct parties manage your transaction during escrow, and each has a specific lane. Confusing their roles leads to misplaced expectations and unnecessary stress.

-

Escrow officer. The escrow officer is a neutral referee who enforces the purchase agreement instructions exactly as written. They collect documents, coordinate the title report, and disburse funds only when all conditions are met. They do not advocate for you, offer legal advice, or negotiate on your behalf.

-

Mortgage lender. Your lender, whether a bank like Wells Fargo, a credit union, or a mortgage broker, funds the loan and sends binding instructions to the escrow officer. After closing, your lender also manages your ongoing mortgage escrow account, collecting monthly amounts for property taxes and homeowners insurance.

-

Real estate agent. Your buyer’s agent coordinates communication between all parties, tracks deadlines, and troubleshoots problems. They are your primary advocate and the person you call when something feels off.

-

Title company. Often working alongside the escrow company, the title company confirms clean ownership and issues title insurance. In California, the buyer typically selects the title and escrow company.

Pro Tip: If you have a legal question about contract terms, do not ask your escrow officer. Hire a real estate attorney or ask your agent to clarify. Escrow officers cannot advise on contract strategy.

Why do monthly mortgage payments change after you close?

Many first-time buyers assume a fixed-rate mortgage means a fixed monthly payment forever. That assumption is wrong, and it catches people off guard within the first year of ownership.

A fixed-rate mortgage does not guarantee a fixed total monthly payment because the escrow portion of your payment covers property taxes and homeowners insurance, both of which fluctuate every year. Your principal and interest payment stays constant, but the escrow portion adjusts annually based on actual tax bills and insurance premiums.

Around 80% of mortgage holders use escrow accounts to spread these costs over 12 months rather than paying large lump sums twice a year. This protects both you and your lender, but it also means your payment is a moving target.

What is an escrow shortage and how does it happen?

An escrow shortage occurs when your lender’s estimate of taxes and insurance at closing turns out to be lower than the actual bills. This is especially common in California, where property taxes are reassessed after a sale at the new purchase price, often significantly higher than the previous owner’s bill.

| Scenario | What happens |

|---|---|

| Property taxes increase after reassessment | Your escrow account runs short; lender sends a shortage notice |

| Homeowners insurance premium rises | Monthly escrow payment increases at next annual review |

| Lender underestimates at closing | Shortage appears within first 12 months |

| You pay lump sum to cover shortage | Monthly payment resets to correct amount going forward |

Escrow shortages are common in the first 12 to 24 months and can be resolved by paying a lump sum or spreading the deficit over the next 12 monthly payments. Neither option is a penalty. It is simply a correction.

Use a mortgage calculator that includes taxes and insurance to model realistic monthly payment scenarios before you close.

How can first-time buyers prepare for escrow challenges in California?

Preparation is the single most effective way to avoid delays and surprises. California’s escrow process has specific requirements that differ from other states, and knowing them in advance puts you ahead.

-

Read every disclosure carefully. California requires sellers to deliver more disclosures than almost any other state. Review your California buyer disclosures line by line before removing your inspection contingency. Disclosures reveal material defects, HOA issues, and neighborhood hazards that affect your decision.

-

Monitor all escrow communications. Respond to emails and document requests from your escrow officer within 24 hours. Delays in returning signed forms are one of the top causes of escrow extensions in California.

-

Clarify your payment estimate with your lender. Ask your lender to show you the escrow analysis worksheet before closing. This document shows the estimated annual tax and insurance amounts and the resulting monthly escrow payment. Compare it against the county assessor’s current tax rate for your target property.

-

Set aside a cash reserve. Budget at least $1,500 to $3,000 beyond your down payment and closing costs for potential escrow shortages in year one. California’s post-sale tax reassessment often creates a shortage notice within the first 12 months.

-

Understand what causes delays. The most common escrow delays in California include appraisal gaps, lender underwriting conditions, title issues from unpermitted work, and slow HOA document delivery. Your agent should flag any of these risks early in the process.

Pro Tip: Ask your agent to request the HOA documents and any permit history from the seller in the first week of escrow. These items take the longest to collect and are the most common source of last-minute delays.

Staying organized throughout escrow also means keeping a folder, physical or digital, with every signed document, wire confirmation, and lender communication. If a dispute arises, your paper trail is your protection. The true cost of homeownership extends well beyond the purchase price, and escrow is where many of those costs first become real.

Key takeaways

The escrow process for first-time buyers in California protects your earnest money, coordinates all parties, and closes your transaction only when every condition is fully satisfied.

| Point | Details |

|---|---|

| Escrow timeline | California escrow typically runs 30 to 60 days from accepted offer to recorded deed. |

| Earnest money protection | Your deposit of 1% to 3% is held securely and applied to closing costs at the end. |

| Escrow officer’s role | They enforce contract terms impartially and cannot offer legal advice or negotiate for you. |

| Payment fluctuations | Fixed-rate loans still have variable monthly payments due to annual tax and insurance adjustments. |

| Shortage readiness | Budget a cash reserve for year-one escrow shortages caused by California’s post-sale tax reassessment. |

What I’ve learned from watching buyers navigate escrow for the first time

The buyers who sail through escrow are not the ones with the most money or the best credit. They are the ones who asked questions early and stayed organized throughout.

The single biggest surprise I see first-time buyers face is the escrow shortage notice that arrives about 10 months after closing. They locked in a fixed-rate mortgage, they budgeted carefully, and then their monthly payment jumps by $150 or $200. They feel misled. They are not. California reassesses property taxes at the new purchase price after every sale, and that reassessment almost always produces a higher bill than the lender estimated at closing. Receiving a shortage notice is routine, not a failure. The lender gives you options, and you move forward.

The second thing I would tell every first-time buyer is this: your escrow officer is not your advisor. They are a neutral administrator. If you receive a document you do not understand, call your agent or a real estate attorney. Do not expect the escrow officer to explain what something means for your situation. That is not their job, and asking them to play that role creates confusion.

Finally, treat every deadline in your purchase contract as non-negotiable. Contingency removal dates, loan approval deadlines, and closing dates all have real financial consequences if missed. Put them in your calendar the day you open escrow. Your agent should be tracking them too, but you are the one with the most at stake.

Escrow is not complicated once you understand the structure. It is a system designed to protect you. Work with it, not around it.

— Anand

Start your home search with Ficustree

Ficustree is an AI-powered real estate platform built specifically for first-time homebuyers in California. From your first property search to the day you get your keys, Ficustree guides you through every step on a single platform, including understanding disclosures, tracking deadlines, and knowing what to expect during escrow. You get hyper-personalized guidance without the overwhelm. Explore the Ficustree buyer platform to see how AI-powered tools can match you with the right home and keep your transaction on track from offer to close.

FAQ

What is escrow in a home purchase?

Escrow is a neutral third-party arrangement where a licensed officer holds your funds and documents until all purchase conditions are met. It protects both the buyer and seller throughout the transaction.

How long does escrow take in California?

The standard escrow period in California runs 30 to 60 days, though cash deals can close faster. Complex transactions involving HOA approvals or title issues may take longer.

What happens to my earnest money during escrow?

Your earnest money deposit is held securely in the escrow account and applied toward your down payment or closing costs at closing. If you cancel within a contingency period, you typically receive it back.

Why did my mortgage payment change after closing?

Your payment changed because the escrow portion, which covers property taxes and homeowners insurance, was adjusted at your annual escrow review. A fixed-rate mortgage keeps your principal and interest constant, but taxes and insurance fluctuate.

What should I do if I receive an escrow shortage notice?

Contact your lender to review your options. You can pay the shortage as a lump sum or spread it across your next 12 monthly payments. Escrow shortages are common in the first two years and are a routine correction, not a penalty.