An FHA loan is a government-insured mortgage that lets first-time homebuyers qualify for home financing with a down payment as low as 3.5% and a credit score around 580. The Federal Housing Administration does not lend money directly. Instead, it insures private lenders against default, which is exactly why those lenders can offer more flexible terms than a standard conventional loan. If you have been told your credit is not strong enough or your savings are too thin, understanding how FHA loans work for first-time buyers may change that picture entirely.

What are the FHA loan eligibility requirements for first-time buyers?

FHA loan guidelines for new buyers center on four main factors: credit score, down payment, debt-to-income ratio, and how you plan to use the property.

Credit score and down payment tiers

The FHA sets two clear credit tiers. Borrowers with a credit score of 580 or higher qualify for the 3.5% minimum down payment. Borrowers with scores between 500 and 579 can still qualify, but the required down payment rises to 10%. Individual lenders often set their own minimums above the FHA floor, so a score of 580 may not be enough at every institution. Always confirm the specific lender’s cutoff before you apply.

Debt-to-income ratio

FHA guidelines generally allow a debt-to-income ratio up to 43%, and some lenders approve borrowers above that threshold with compensating factors like strong cash reserves. This is notably more flexible than most conventional loan programs, which cap DTI closer to 36% to 45% with stricter conditions. Your total monthly debt payments, including the new mortgage, are divided by your gross monthly income to produce this number.

Owner-occupancy and income requirements

The FHA requires the home to be your primary residence. You cannot use an FHA loan to buy a vacation property or a rental investment. Lenders will also verify steady employment and consistent income through pay stubs, W-2s, and tax returns, typically covering the past two years.

Pro Tip: If your credit score sits between 560 and 579, spending three to six months paying down revolving balances could push you above 580 and cut your required down payment by more than half.

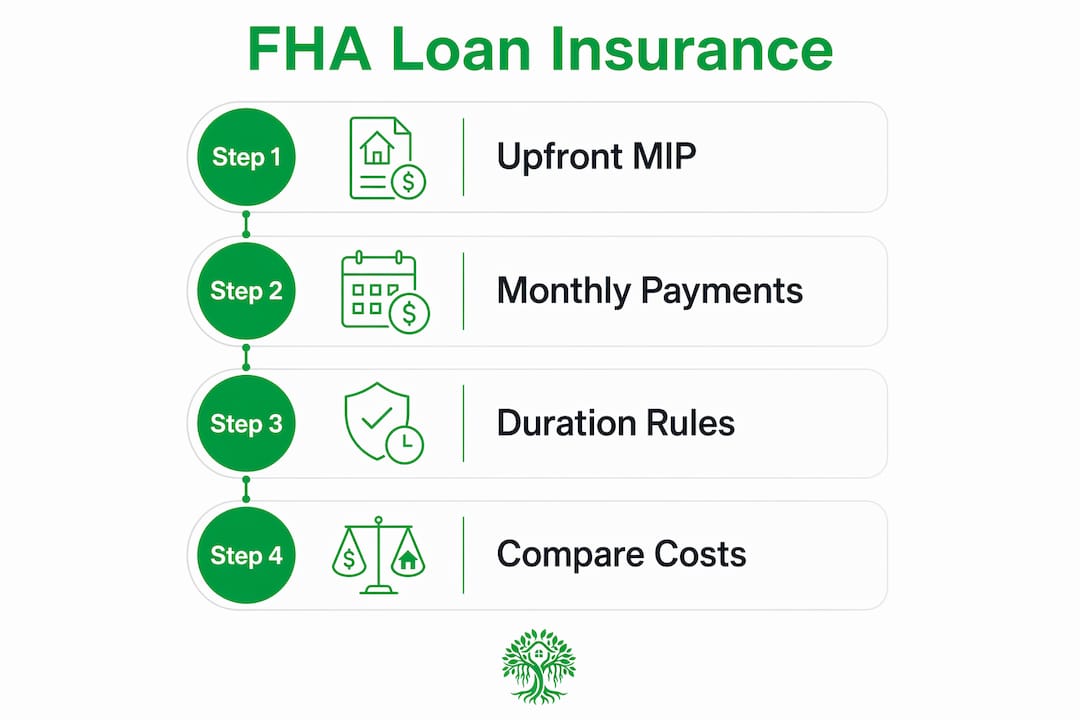

How do mortgage insurance premiums affect FHA loans?

Mortgage insurance is the trade-off for FHA’s flexible entry requirements, and it affects your monthly payment more than most first-time buyers expect.

Every FHA loan carries an upfront mortgage insurance premium of 1.75% of the loan amount, which is typically rolled into the loan balance rather than paid at closing. On a $300,000 loan, that adds $5,250 to what you owe from day one. Beyond that, you pay an annual MIP ranging from 0.40% to 0.85% of the loan balance, divided across your monthly payments.

The duration of MIP is where FHA loans diverge sharply from conventional mortgages. If your down payment is under 10%, MIP lasts for the life of the loan. Put down 10% or more, and MIP cancels after approximately 11 years. Conventional loans with private mortgage insurance (PMI) automatically cancel once you reach 20% equity, which can make conventional financing cheaper over a long horizon even if the entry bar is higher.

| Feature | FHA loan | Conventional loan |

|---|---|---|

| Upfront insurance cost | 1.75% of loan amount | None |

| Annual insurance rate | 0.40% to 0.85% | 0.20% to 1.50% (varies) |

| Insurance cancellation | Life of loan (under 10% down) | At 20% equity automatically |

| Minimum credit score | ~500 to 580 | Typically 620+ |

| Minimum down payment | 3.5% | 3% to 5% (varies by program) |

The total monthly payment on an FHA loan includes principal, interest, MIP, property taxes, and homeowner’s insurance. Focusing only on the down payment misses the real affordability picture. Use a mortgage calculator with taxes and insurance to model the full monthly cost before you commit.

Pro Tip: If you plan to stay in the home long-term, run a side-by-side comparison of FHA vs. conventional total costs over seven years using the payment differences between both loan types. The lower FHA entry cost sometimes loses to conventional savings on insurance over time.

What is the FHA loan application and home buying process?

The first-time homebuyer FHA loan process follows a clear sequence. Knowing each step in advance prevents surprises that delay closing.

-

Find an FHA-approved lender. Not every bank or mortgage company participates in the FHA program. The U.S. Department of Housing and Urban Development (HUD) maintains a searchable lender list. Compare at least three Loan Estimates, focusing on the APR and total monthly payment rather than just the interest rate.

-

Get pre-approved. Submit your income documents, bank statements, tax returns, and authorization for a credit pull. Pre-approval tells you exactly how much you can borrow and signals to sellers that you are a serious buyer.

-

Make an offer and open escrow. Once a seller accepts your offer, the transaction moves into escrow and your lender orders an FHA appraisal.

-

Pass the FHA appraisal. This is the step that surprises most first-time buyers. The FHA appraisal checks both market value and HUD Minimum Property Requirements (MPRs). Common issues that trigger required repairs include electrical hazards, roof damage, missing handrails, and structural problems. The home must meet safety, security, and soundness standards before the loan can close.

-

Complete underwriting. Your lender reviews all documents, verifies the source of your down payment, and confirms the property meets FHA standards. If your down payment includes gift funds or down payment assistance, proper documentation such as a gift letter and bank transfer records is mandatory. Missing paperwork at this stage is one of the most common causes of closing delays.

-

Close on the home. Once underwriting issues a clear-to-close, you sign final documents, pay closing costs, and receive the keys.

Pro Tip: Ask your real estate agent to include an FHA repair addendum in your offer. This gives you and the seller a clear framework for handling appraisal-required repairs without renegotiating the entire contract.

The full process from pre-approval to closing typically runs 30 to 60 days. FHA appraisal repairs can extend that timeline, so build in buffer time if you have a firm move-in date. For a broader look at every step involved, the first-time homebuyer guide from Ficustree walks through the full process in plain language.

Are FHA loans only for first-time buyers?

This is one of the most persistent myths in residential lending. FHA loans are not limited to first-time buyers. They are heavily marketed to first-time buyers because the low down payment and flexible credit requirements align with where many new buyers start financially. Eligibility, however, is based entirely on your financial profile and the property you are buying, not on whether you have owned a home before.

A repeat buyer who sold their previous home, has a credit score of 600, and wants to put down 3.5% on a new primary residence qualifies for an FHA loan. The key restrictions are:

- The property must be your primary residence, not a second home or investment property.

- You must meet the credit, income, and DTI requirements at the time of application.

- The property must meet HUD’s Minimum Property Requirements.

- You generally cannot carry two FHA loans simultaneously unless specific exceptions apply, such as relocating for work.

Understanding this distinction matters if you are planning a repeat purchase or transitioning from renting to owning after a period of homeownership. The FHA program rewards financial readiness, not first-time status.

What are the most important tips for first-time FHA loan borrowers?

Knowing the rules is one thing. Applying them to your specific situation is where most buyers need practical guidance.

-

Document every dollar of your down payment. Whether your funds come from savings, a family gift, or a state down payment assistance program, your lender needs a paper trail. Gift funds require a gift letter and bank records showing the transfer. Down payment assistance programs require their own documentation package. Start gathering this early.

-

Factor MIP into your budget from day one. FHA loans carry higher monthly costs than conventional loans due to ongoing mortgage insurance. Use the home affordability calculator at Ficustree to model your real monthly payment including MIP, taxes, and insurance before you set your price range.

-

Compare multiple lenders. FHA sets the floor on rates and requirements, but lenders set their own pricing above that floor. Two lenders offering the same FHA loan can have meaningfully different APRs. Request Loan Estimates from at least three lenders and compare them line by line.

-

Negotiate repair costs with the seller. If the FHA appraisal flags required repairs, you have options. You can ask the seller to complete the repairs before closing, request a price reduction to cover your repair costs, or in some cases use an FHA 203(k) rehabilitation loan to finance repairs into the mortgage.

-

Plan your refinance exit. If you put down less than 10%, MIP stays with your loan permanently unless you refinance into a conventional mortgage after building equity. Many buyers refinance once they reach 20% equity to eliminate the insurance cost entirely. Build this into your long-term financial plan from the start.

Pro Tip: Check your state’s housing finance agency website before you apply. Most states offer down payment assistance programs specifically for FHA borrowers that can cover part or all of the 3.5% requirement. Many buyers leave this money on the table simply because they did not know to look.

For a full picture of what homeownership actually costs beyond the mortgage, the true cost of homeownership breakdown from Ficustree is worth reading before you finalize your budget.

Key takeaways

FHA loans give first-time buyers access to affordable mortgages by trading flexible entry requirements for mandatory mortgage insurance that can last the life of the loan.

| Point | Details |

|---|---|

| Government insurance enables access | FHA insures lenders against default, allowing lower credit and down payment thresholds than conventional loans. |

| Two credit tiers determine your down payment | A score of 580 or higher means 3.5% down; scores from 500 to 579 require 10% down. |

| MIP adds real monthly cost | Upfront MIP of 1.75% plus annual premiums of 0.40% to 0.85% increase your total payment significantly. |

| Appraisal standards can affect closing | FHA appraisals check HUD safety and soundness requirements; required repairs can delay your timeline. |

| FHA is not exclusive to first-time buyers | Any qualified borrower buying a primary residence can use an FHA loan, regardless of prior ownership history. |

Why FHA loans still make sense in 2026, even with the MIP trade-off

By Anand

After working with hundreds of first-time buyers, the single biggest misconception I see is that FHA loans are a consolation prize for buyers who cannot qualify for anything better. That framing is wrong, and it costs people money.

FHA’s government backing is a genuine structural advantage. It opens the door to homeownership years earlier than waiting to save a 20% conventional down payment would allow. For buyers in markets where rents are rising faster than savings can accumulate, that time advantage is real and measurable.

That said, two things consistently catch buyers off guard. First, the MIP duration. Most buyers assume mortgage insurance works like PMI on a conventional loan and cancels automatically at 20% equity. It does not on FHA loans with under 10% down. I have seen buyers five years into a loan still paying MIP they thought would be gone by year three. Know this going in, and plan your refinance timeline accordingly.

Second, the appraisal repair requirement. FHA appraisers are not just valuing the property. They are inspecting it against HUD’s safety and soundness standards. A seller who has deferred maintenance on the roof or electrical panel may not be willing to fix it before closing. This is where having a knowledgeable FHA lender and a buyer’s agent who has closed FHA deals before makes a real difference. They know how to structure the repair negotiation without blowing up the deal.

My honest advice: use FHA to get in, build equity, then refinance to conventional when you hit 20%. That sequence works. What does not work is treating FHA as a permanent mortgage without a plan to exit the MIP.

— Anand

How Ficustree helps you navigate FHA home buying

Ficustree is an AI-powered platform built specifically for first-time buyers, and it covers the full path from home search to closing in one place. When you are comparing FHA loan options, Ficustree matches you with lenders, helps you model total monthly costs including MIP, and guides you through every document and decision point along the way. You do not need to piece together advice from a dozen different websites. The platform gives you a personalized experience that adapts to your credit profile, budget, and timeline. Explore what Ficustree can do for your FHA home search and see how much clearer the process gets when everything is in one place. Learn more about the platform at ficustree.ai.

FAQ

What credit score do I need for an FHA loan?

You need a minimum credit score of 580 to qualify for the 3.5% down payment option, or a score between 500 and 579 with a 10% down payment. Individual lenders may set higher minimums, so confirm requirements directly with your lender.

How long does FHA mortgage insurance last?

If your down payment is under 10%, FHA mortgage insurance lasts for the life of the loan. A down payment of 10% or more reduces MIP to approximately 11 years. Refinancing into a conventional loan after reaching 20% equity is the most common way to eliminate it early.

Can I use gift money for my FHA down payment?

Yes. FHA allows gift funds from family members and down payment assistance programs, but your lender requires a gift letter and documentation of the bank transfer. Missing paperwork is one of the most common causes of underwriting delays.

What does an FHA appraisal check?

An FHA appraisal evaluates both the market value of the home and HUD’s Minimum Property Requirements covering safety, security, and soundness. Common issues that require repair before closing include electrical hazards and roof damage, as well as structural problems.

Are FHA loans only available to first-time buyers?

No. FHA loans are available to any qualified borrower purchasing a primary residence, including repeat buyers who qualify. The program is popular with first-time buyers because of its flexible requirements, but ownership history is not part of the eligibility criteria. For more on FHA eligibility details, the FHA loan FAQs resource covers credit, down payment, and qualification questions in depth.