A title company in real estate is the neutral third party responsible for verifying legal ownership, managing closing funds, and guaranteeing that property transfers to you free of hidden claims. Every residential and commercial transaction depends on this function. Whether you are buying your first home or adding to an investment portfolio, understanding the role of title company real estate professionals play protects your money and your ownership rights from day one.

What does a title company do in a real estate transaction?

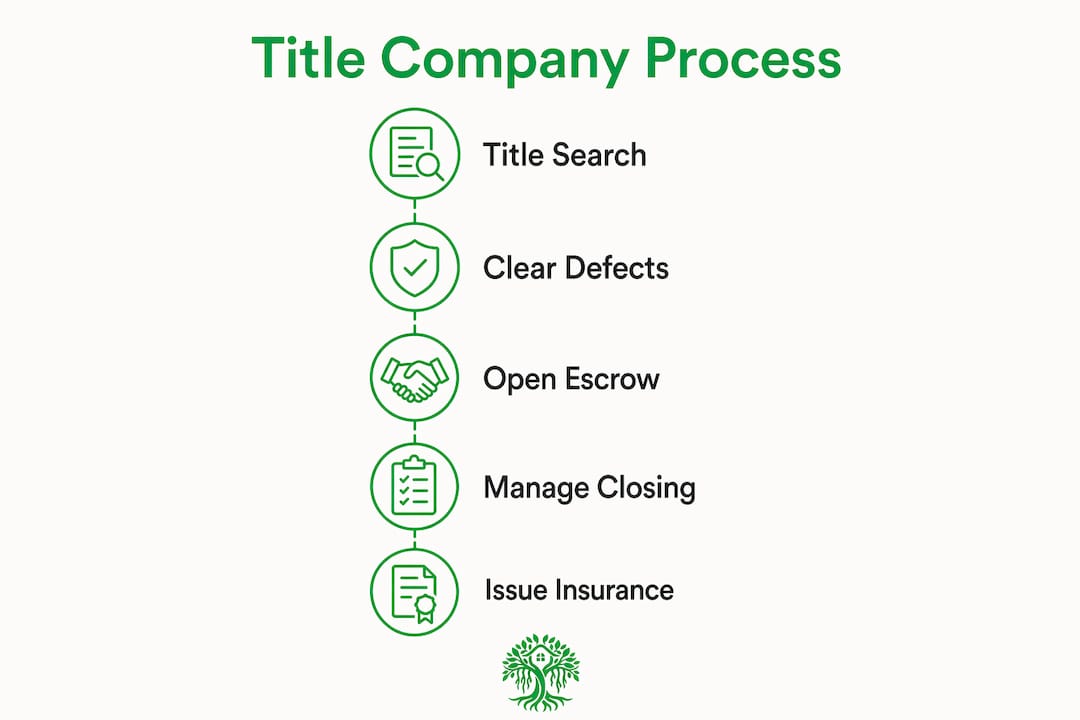

A title company serves as the operational backbone of any property sale, handling four core functions: title research, escrow management, closing coordination, and title insurance issuance. Title company work is a comprehensive risk-management process that runs before, during, and after closing. Most buyers only see the company at the closing table, but the real work starts weeks earlier.

The company’s first job is confirming that the seller actually owns the property and has the legal right to sell it. This sounds straightforward, but property records stretch back decades, sometimes centuries, and errors accumulate. Liens from unpaid contractors, judgments from old lawsuits, and improperly recorded deeds can all cloud ownership. The title company finds these problems before they become your problems.

Once ownership is verified, the company opens an escrow account, collects funds from the buyer and lender, and holds everything in trust until every closing condition is satisfied. At closing, it prepares and reviews all documents, coordinates signatures, and disburses funds to every party. After closing, it records the new deed and mortgage with the county and delivers your title insurance policy.

What does the title search involve and why is it critical?

The title search is the foundation of every clean real estate closing. A title examiner traces the chain of title, reviewing public records to confirm an unbroken line of ownership from the original grant to the current seller. Title defects typically appear during this detailed search, not at the offer stage, which is why starting early matters.

Here is what the title search uncovers:

- Liens and judgments. Unpaid contractor bills, IRS tax liens, and court judgments attach to property and must be paid off before or at closing.

- Easements and encroachments. A neighbor’s driveway crossing your lot or a utility easement can restrict how you use the land.

- Ownership gaps. A missing heir, a forged signature on a past deed, or an estate that was never properly settled can break the chain of title.

- Unpaid property taxes. Back taxes follow the property, not the seller. You could inherit a tax bill if the search misses it.

- Mis-recorded documents. A deed filed in the wrong county or with a misspelled name can create legal ambiguity that takes weeks to resolve.

Each defect found must be cleared before closing. The title company contacts sellers, lenders, and attorneys to resolve exceptions. Missing releases get obtained. Liens get paid. Corrective deeds get filed. Understanding why title search matters before you close can save you from inheriting someone else’s financial dispute.

Pro Tip: Submit your vesting information and contract terms to the title company as early as possible. Seasoned buyers who provide accurate details upfront give the examiner time to clear exceptions before closing, avoiding last-minute delays that can push your move-in date back by days or weeks.

How do title companies manage escrow and facilitate the closing process?

Escrow management is where the title company’s role shifts from researcher to financial custodian. Title companies serve as escrow agents holding funds securely and managing disbursement only after all closing conditions are met. One critical distinction: this escrow account is separate from the mortgage servicer escrow that handles your future tax and insurance payments. The title company escrow strictly holds closing and sale funds until the transaction is complete.

The closing coordination process follows a clear sequence:

- Open escrow. The title company receives the signed purchase agreement and opens an escrow account. Earnest money deposits go in first.

- Collect lender instructions. The lender sends a closing package specifying exactly how funds must be disbursed and what documents must be signed.

- Prepare the Closing Disclosure. The title company prepares and reconciles settlement statements, ensuring title charges and insurance fees match lender requirements. This document lists every dollar flowing in and out of the transaction.

- Conduct the closing. All parties sign the deed, mortgage, and loan documents. A notary witnesses signatures. The title company confirms every document is complete and correctly executed.

- Disburse funds. Once the lender releases funds, the title company pays the seller, satisfies existing mortgages, pays real estate agents their commissions, and covers all closing costs and fees.

- Record the deed. The company files the new deed and mortgage with the county recorder, officially transferring ownership.

Errors in fund disbursement can cause serious legal complications for all parties. A single transposed account number or a missed lien payoff can unwind an entire closing. This is why reviewing your Closing Disclosure carefully before the closing date is non-negotiable.

Pro Tip: Review your settlement statement at least 24 hours before closing. Compare every line item against your Loan Estimate. If a title fee increased or a new charge appeared, ask the title company for a written explanation before you sign anything.

What is title insurance and how does it protect buyers and lenders?

Title insurance protects buyers and lenders from financial loss due to undiscovered title defects that surface after the sale closes. Unlike homeowner’s insurance, which covers future events, title insurance covers past events that were not discovered during the title search. You pay a one-time premium at closing, and the coverage lasts as long as you own the property.

There are two distinct policies:

- Owner’s title insurance. This protects your financial interest in the property. If a long-lost heir files a claim against your ownership two years after closing, your policy covers legal defense costs and any financial loss up to the policy amount. It is technically optional in most states but strongly recommended.

- Lender’s title insurance. This protects the mortgage lender’s interest in the property. Nearly every lender requires it as a condition of the loan. The buyer pays for it, but it only protects the lender.

Before issuing either policy, the title company issues a title commitment document. This document outlines what the policy will cover, what it excludes, and what conditions must be met before coverage takes effect. The title commitment sets coverage expectations and requires good communication between all parties to keep the transaction on schedule.

Common title defects covered by insurance include forged deeds, undisclosed heirs, errors in public records, and boundary disputes. Common exclusions include defects you created yourself, zoning violations you were aware of, and environmental hazards. After closing, title companies send the final policies to buyers and lenders. Store yours in a safe place. You may need it years from now.

Why is recording the deed essential and what role does the title company play?

Recording the deed is the true legal milestone of ownership transfer, not the moment you sign at the closing table. Until the deed is recorded with the county recorder’s office, the transfer is not public knowledge, which means a dishonest seller could theoretically sell the same property to someone else. The title company coordinates closings so funds disburse only when recording can proceed smoothly.

The title company’s recording responsibilities include:

- Filing the deed. The company submits the executed deed to the county recorder, paying the required recording fees.

- Filing the mortgage or deed of trust. The lender’s security interest must also be recorded to be legally enforceable.

- Confirming receipt. The company tracks the filing and confirms the county has stamped and indexed the documents correctly.

- Notifying all parties. Once recording is confirmed, the title company notifies the buyer, seller, lender, and agents that the transaction is officially complete.

State-specific practices add complexity here. In some states, attorneys participate in closing or document preparation, while title companies still handle most title and escrow duties. In California, for example, escrow companies and title companies often operate as separate entities, though many buyers work with a combined service. Confirm local customs before closing so you understand who is responsible for what and what fees apply. The escrow process for first-time buyers in California has specific nuances worth understanding before you reach the closing table.

Key takeaways

A title company’s role in real estate spans the entire transaction, from ownership verification and escrow management to closing facilitation, title insurance issuance, and deed recording.

| Point | Details |

|---|---|

| Title search protects ownership | The search uncovers liens, gaps, and defects before they transfer to the buyer. |

| Escrow keeps funds secure | The title company holds all closing funds in trust and disburses only when conditions are met. |

| Two types of title insurance | Owner’s policies protect buyers; lender’s policies protect the mortgage lender. Both are issued at closing. |

| Recording finalizes the transfer | The deed and mortgage must be filed with the county to make ownership legally public and enforceable. |

| State rules vary | Some states require attorneys at closing; confirm local practices to avoid unexpected fees or delays. |

What I’ve learned about title companies that most buyers miss

Most buyers treat the title company as a formality, a box to check on the way to getting keys. That mindset costs people time and money. The title company is the only party in a real estate transaction with no financial stake in whether the deal closes. Your agent earns a commission when it closes. Your lender earns origination fees when it closes. The title company gets paid either way, which makes it the most objective set of eyes in the room.

I have seen transactions fall apart two days before closing because a lien from a 15-year-old home equity line was never formally released. The seller thought it was paid off. The bank thought it was paid off. The title search proved otherwise. A diligent title company caught it, tracked down the release, and saved the deal. That is not paperwork. That is risk management.

The single most underrated factor when choosing a title company is lender relationships. Experienced title companies with strong lender relationships facilitate smoother closings by reducing delays and errors. When a title officer and a loan processor have worked together on 200 closings, they communicate faster, catch discrepancies earlier, and solve problems before they escalate. Ask your agent which title companies they have seen perform well under pressure, not just which ones offer the lowest fees.

One more thing: do not ignore the title commitment document when it arrives. Most buyers file it away unread. That document tells you exactly what your insurance will and will not cover. Reading it takes 20 minutes and can prevent a very expensive surprise years down the road.

— Anand

How Ficustree helps you navigate the closing process with confidence

Understanding every step of a real estate transaction is exactly what Ficustree was built for. The platform guides first-time buyers from property search through closing on a single AI-powered platform, so you always know what is coming next and why it matters.

Ficustree’s tools give you hyper-personalized guidance on transaction milestones, including how to work with your title company, what to review before closing, and how to protect your ownership rights after the deal is done. You do not have to figure this out alone. Start your home search with Ficustree and get the support you need from search to settlement.

FAQ

What is the main role of a title company in real estate?

A title company verifies legal ownership, manages escrow funds, facilitates closing, issues title insurance, and records the deed with the county. Its core function is ensuring the buyer receives clean, unencumbered ownership.

Is title insurance required when buying a home?

Lender’s title insurance is required by nearly all mortgage lenders. Owner’s title insurance is technically optional in most states but strongly recommended, since it protects your financial interest against past defects that surface after closing.

How long does a title search take?

A title search typically takes a few days to two weeks, depending on the property’s history and local record-keeping systems. Complex ownership histories or unresolved liens can extend the timeline.

What happens if a title defect is found after closing?

Your owner’s title insurance policy covers legal defense costs and financial losses up to the policy amount if a covered defect surfaces after closing. This is why storing your policy documents safely is so important.

Can you choose your own title company?

Yes. In most states, buyers have the right to choose their title company. Comparing experience, lender relationships, and fee structures before selecting one can meaningfully affect how smoothly your closing goes.