A title search is a detailed examination of public records confirming the legal ownership and any existing claims on a property, giving buyers proof they will receive clear title free of liens or disputes. For first-time homebuyers in California, understanding why title search matters when buying a home is the difference between a clean closing and a legal nightmare that can surface months or years after you move in. Nearly 35% of real estate transactions encounter title-related issues before closing. That number means your deal has a one-in-three chance of hitting a problem that could delay or kill the sale. Knowing what a title search does, how it works in California, and how it pairs with title insurance puts you in control from day one.

Why title search matters when buying a home

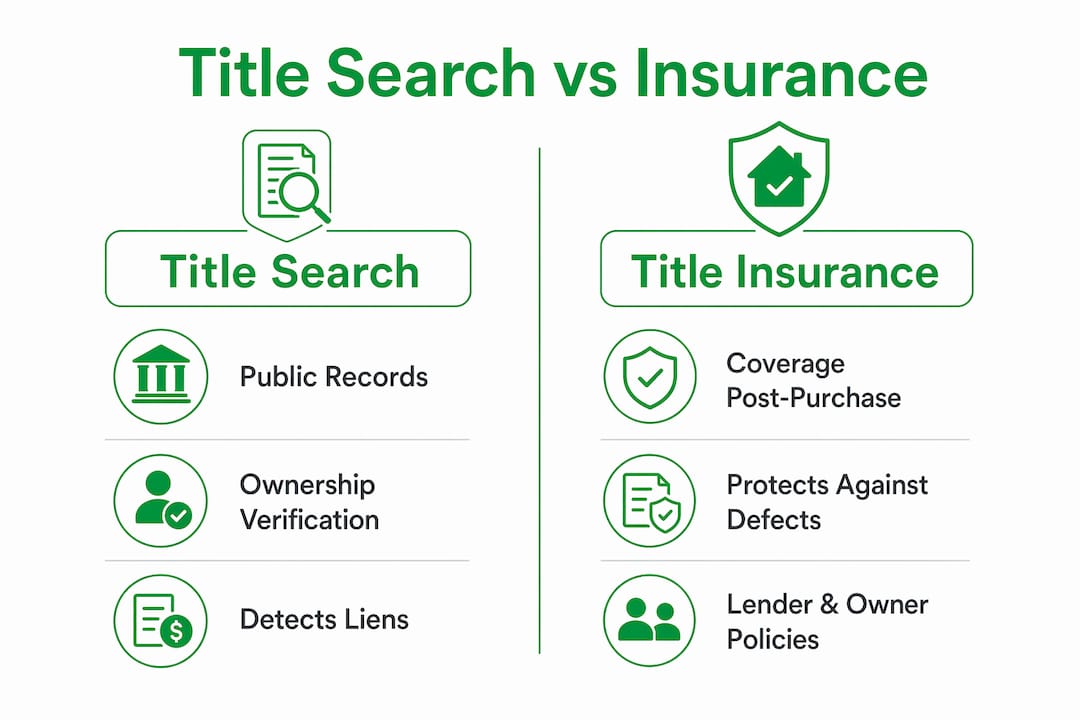

A title search confirms the seller’s legal right to sell and reveals any liens, unpaid taxes, easements, or ownership disputes attached to the property. Think of it as a background check on the home itself, not just the seller. Without it, you could close on a house only to discover a contractor placed a lien on it two years ago for unpaid work, and that debt is now yours to resolve.

The industry term for what you are verifying is a marketable title. A marketable title is one free from reasonable doubt or adverse claims, and uncovering issues before closing avoids costly post-sale litigation. California’s real estate market moves fast, and escrow periods can be as short as 21 days in competitive areas like the Bay Area or Los Angeles. That compressed timeline makes early title review non-negotiable.

Your lender will almost always require a title search before approving your mortgage. But the importance of title search goes beyond satisfying the bank. It protects your equity, your ownership rights, and your ability to sell or refinance the home in the future.

How does a title search work in California home purchases?

Title searches in California are conducted by licensed title companies such as Fidelity National Title, First American Title, or Old Republic Title. These companies work alongside escrow agents to review public records before your closing date. The process follows a clear sequence.

- Order the search. Your escrow officer or real estate agent orders the title search shortly after your offer is accepted. In California, this typically happens within the first few days of opening escrow.

- Public records review. The title examiner searches county recorder records, court judgments, tax records, and federal and state tax liens. They look at every deed, mortgage, and legal action tied to the property’s chain of ownership.

- Preliminary title report. The title company issues a preliminary report listing all findings. Your escrow officer reviews this with you and flags any items that need to be resolved before closing.

- Clearing exceptions. If the report shows an old lien or an unresolved easement, the seller must address it before the transaction can proceed. This step is where deals can slow down.

- Title insurance issued. Once the title is cleared, the title company issues insurance policies at closing.

In 2026, a standard title search costs between $75 and $300 and takes anywhere from a few days to two weeks. That timeline matters because a delayed search can push your closing date past your mortgage rate lock, potentially costing you thousands in higher interest. Digital title search platforms can reduce search time from days to minutes by cross-referencing multiple records simultaneously, cutting the risk of delays that threaten your rate lock.

Pro Tip: Ask your escrow officer on day one whether they use a digital title search platform. If they rely on manual county records, factor in extra buffer time before your rate lock expires.

What common issues can title searches uncover?

Title defects range from minor paperwork errors to serious ownership disputes. Each one has the potential to cloud your ownership rights if left unresolved. Here are the most common problems a title search surfaces:

- Unpaid liens. Contractors, subcontractors, or suppliers who were never paid can file mechanic’s liens against a property. The average lien discovered during a title search is valued at $4,900. That is a debt you would inherit at closing if the search missed it.

- Unpaid property taxes. Delinquent tax bills attach to the property, not the owner. California counties can initiate tax default proceedings if taxes go unpaid long enough, putting your ownership at risk.

- Easements and deed restrictions. A neighbor may have a legal right to cross your property, or a deed restriction from 1952 may prohibit adding a second unit. These do not block the sale but directly affect how you can use the land.

- Ownership disputes. Divorces, probate cases, and family disagreements can leave competing claims on a property. If a deceased prior owner’s heir was never properly bought out, that heir may have a legal claim to your home.

- Forged or fraudulent documents. Deed fraud is a real and growing problem. A forged deed in the chain of title can invalidate the seller’s ownership entirely.

- Judgment liens. If a prior owner lost a lawsuit and never paid the judgment, that creditor may have filed a lien against the property.

“Title problems often arise from decades-old issues like unpaid taxes or disputed heirs attached to the property, not the seller, becoming the buyer’s responsibility if unresolved.” — Rocket Mortgage

The consequences of missing these issues are severe. You could face a lawsuit from an unknown heir, lose the ability to refinance because the title is clouded, or spend tens of thousands in legal fees clearing a lien you did not know existed. Reviewing your California buyer disclosures alongside the preliminary title report gives you the fullest picture of what you are actually buying.

Title search vs. title insurance: how they complement each other

A title search and title insurance are not the same thing, and you need both. The search looks backward through history to find known problems. Title insurance protects you forward against problems the search may have missed.

| Feature | Title search | Title insurance |

|---|---|---|

| What it does | Reviews public records for existing claims | Covers losses from defects not found in the search |

| When it happens | Before closing | Purchased at closing |

| Duration of protection | One-time review | Lifetime of ownership (owner’s policy) |

| Cost | $75 to $300 | 0.4% to 0.7% of purchase price |

| Who it protects | Informs buyer and lender | Buyer (owner’s policy) or lender (lender’s policy) |

Title insurance protects buyers from ownership defects discovered after purchase, such as forged deeds or undisclosed heirs that the search may have missed. The owner’s policy is a one-time fee paid at closing and remains effective for as long as you or your heirs own the home. That is a significant benefit for a relatively modest cost.

Lender’s title insurance protects only the lender. Your mortgage lender will require their own policy, but that policy covers the bank’s investment, not yours. If a title defect surfaces after closing, the lender’s policy pays the bank. You are left to fight the legal battle on your own without an owner’s policy. This distinction is one of the most misunderstood aspects of the home buying process, and it catches first-time buyers off guard regularly.

Pro Tip: In California, the seller traditionally pays for the owner’s title insurance policy in many counties, but this is negotiable. Confirm who pays during your offer negotiations so there are no surprises at closing.

The true cost of homeownership includes title insurance as a line item you should plan for. On a $700,000 home in California, an owner’s policy runs roughly $2,800 to $4,900. That is a small price compared to the cost of defending your ownership in court.

Practical tips for California first-time homebuyers on title searches

Knowing the process is one thing. Executing it well under the pressure of a live transaction is another. These steps will help you stay ahead of title issues from offer to close.

- Order the search immediately after acceptance. Do not wait for your lender to prompt you. Ask your real estate agent or escrow officer to initiate the title search the same day your offer is accepted.

- Read the preliminary title report carefully. This document lists every exception to clear title. Ask your escrow officer to walk you through each item in plain language.

- Verify the chain of title goes back at least 40 years. California courts generally require a 40-year search to establish marketable title. Confirm your title company meets this standard.

- Ask specifically about easements. Easements in California can affect your ability to build an ADU (accessory dwelling unit), add a fence, or expand the home. These are legal and binding even if the seller was unaware of them.

- Do not skip the owner’s title insurance policy. Even if your lender does not require it, purchase an owner’s policy. Skipping title searches or insurance can mean inheriting unpaid taxes, liens, or competing ownership claims with no recourse.

If the preliminary report reveals a problem, here is what to do:

- Request that the seller resolve the issue before closing. Most purchase contracts in California require the seller to deliver clear title.

- Ask your escrow officer for a timeline. Clearing a lien or resolving a probate issue can take days or weeks.

- Consult a real estate attorney if the issue involves a disputed ownership claim or a forged document.

- Use a first-time homebuyer guide to understand how title issues fit into the broader closing timeline.

Cash buyers face a specific risk worth calling out. Buyers using cash or owner financing may skip the title search entirely because no lender is requiring it. This is one of the costliest mistakes a buyer can make. Without a lender’s requirement as a safety net, the responsibility to order the search falls entirely on you.

Key takeaways

A title search is the single most important due diligence step in a California home purchase because it verifies legal ownership and surfaces liens, disputes, and defects that become the buyer’s problem at closing.

| Point | Details |

|---|---|

| Title search is non-negotiable | It confirms the seller’s legal right to sell and protects your ownership from day one. |

| California searches follow a clear process | Escrow opens, public records are reviewed, a preliminary report is issued, and exceptions must be cleared before closing. |

| Common defects include liens and disputes | The average lien found is $4,900; ownership disputes and forged deeds can invalidate your purchase entirely. |

| Owner’s title insurance fills the gaps | The search finds known issues; the owner’s policy covers defects the search missed, for the life of your ownership. |

| Cash buyers must self-initiate | Without a lender requirement, cash buyers must order the search themselves or accept all historical risks. |

Why I think most first-time buyers underestimate title risk

Most buyers I have seen go through the process treat the title search as a formality, something the escrow officer handles in the background while they focus on inspections and loan approvals. That mindset is a mistake.

The cases that stick with me are the ones involving decades-old problems. A buyer in the East Bay purchased a home only to discover a mechanic’s lien from a remodel done 11 years prior. The contractor had gone out of business, but the lien was still valid and recorded. The seller had no idea it existed. Clearing it added three weeks to the closing timeline and nearly blew up the rate lock.

Technology is genuinely changing this. Digital title platforms that cross-reference county records, court judgments, and tax databases in minutes are reducing the window for human error. But the technology only helps if your escrow team is using it. Ask the question directly.

My honest advice: treat the preliminary title report like a home inspection report. Read every line. Ask about every exception. Do not assume your escrow officer will flag everything that matters to you personally, because their job is to clear the title for closing, not to advise you on how an easement affects your renovation plans.

The cost of an owner’s title insurance policy is one of the best dollars you will spend in the entire transaction. The search finds what is known. The insurance covers what is not.

— Anand

Start your home search with title clarity built in

Ficustree is an AI-powered platform built specifically for first-time homebuyers in California, guiding you from your first search through closing on a single platform. When you find a property you love, Ficustree surfaces key property data and flags potential title-related considerations so you walk into escrow informed, not surprised. You get hyper-personalized guidance at every step, including help understanding what your preliminary title report means and what questions to ask your escrow officer. Start your search with confidence at ficustree.ai and let the platform do the heavy lifting so you can focus on finding your dream home.

FAQ

What is a title search when buying a home?

A title search is a review of public records, including deeds, court judgments, tax records, and liens, to confirm the seller legally owns the property and that no claims exist that could affect the buyer’s ownership.

How long does a title search take in California?

A standard title search takes a few days to two weeks, though digital platforms can complete the process in minutes. Delays in the search can push your closing date past your mortgage rate lock.

Do I need title insurance if a title search was already done?

Yes. A title search finds known issues in public records, but title insurance covers defects that the search missed, such as forged deeds or undisclosed heirs. The owner’s policy protects you for the entire time you own the home.

What happens if a title search finds a problem?

Your escrow officer will list the issue as an exception on the preliminary title report. In California, the seller is typically required to resolve title defects before closing. If the issue is complex, a real estate attorney should be consulted.

Can I skip the title search if I am paying cash?

You can, but it is a serious risk. Cash buyers who skip the title search accept all historical claims on the property, including unpaid taxes, liens, and competing ownership disputes, with no lender requirement to catch them.